- We expect the RBA will leave Australia’s cash rate unchanged at 4.35% in May

- Updated forecasts may show underlying inflation returning to its target band later than 2025

- Its tone towards on inflation outlook is likely to be more hawkish than six weeks ago

- RBA likely to repeat it isn’t ruling “anything in or out” while reinforcing that means rates may go higher

- Signs of increased hawkishness may underpin further AUD gains

RBA cash rate set to remain at 4.35%

We expect the RBA will leave the cash rate steady at 4.35% with the risk of guidance in the final paragraph of the statement reintroducing the specific risk of further rate hikes being required.

Inflation forecasts set to be revised higher, unemployment lower

In what will be a comprehensive update with not only the monetary policy statement but also updated quarterly economic forecasts and press conference from Governor Michele Bullock, traders should be focusing on is what the RBA will say and project about the future path of inflation as that will largely determine what it does with interest rates.

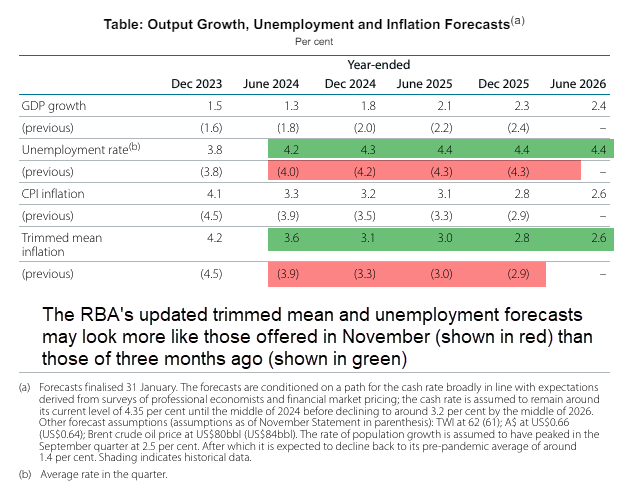

After underlying inflation came in two tenths hotter than expected in the March quarter, it’s likely its trimmed mean inflation forecast for June 2024 will be upgraded by the same amount to 3.8%. However, it’s the longer-term projections that will move markets with a string of upgrades for 2025 and 2026 likely to increase the risk of the next move in the cash rate being higher.

In February, the RBA forecast trimmed mean inflation would decelerate to 3.1% by end-2024 and 2.8% by end-2025, with inflation only returning to the midpoint of its 2-3% target (which is effectively its new mandate under the updated monetary policy framework signed late last year) by the middle of 2026.

Source: RBA

Key forecast parameters

Those forecasts were created under the assumption rate cuts would begin in the second half of 2024, a more dovish assessment to that of today where markets expect the first rate cut of the cycle will occur in the June quarter next year. To some, the higher rates projection limits the risk of the RBA pushing its entire underlying inflation forecasts higher, an outcome that may be perceived as dovish given markets are flirting with the idea of the bank hiking interest rates again this year.

However, with unemployment holding at 3.8%, it’s likely the RBA will have to lower its near-term forecasts given it previously saw unemployment hitting 4.2% by the middle of 2024. With its forecasts for the AUD, Brent crude, population projections and GDP growth likely to be similar to three months ago, that will create an offsetting factor to the higher rates profile, pointing to the risk of the bank showing a slower return to the midpoint of its inflation target.

When you consider the stickiness of domestic inflationary pressures in the March quarter report, the updated trimmed mean inflation and unemployment projections could look something similar to those issued in November when the RBA last hiked rates.

Inflation tone set to be more hawkish

Mirroring risks to the inflation forecasts, the board’s tone on the inflation outlook may come across as more hawkish than six weeks ago. It will be difficult for the bank to repeat that “recent information suggests that inflation continues to moderate, in line with the RBA’s latest forecasts” given its forecasts were easily exceeded in the March quarter.

While the statement remains factually true, its view that services inflation “remains elevated, and is moderating at a more gradual pace” may be altered given just how far above target services inflation current sits.

It will likely repeat the inflation data is “consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs”.

RBA may acknowledge slow progress on inflation target

In the key final paragraph of the policy statement, it would not surprise if the RBA were to reflect on the slow pace that inflation is returning to its target. It’s not just “high” but stubbornly high right now.

While it will likely repeat the “path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain" and that it is "not ruling anything in or out”, refraining from reinserting the phrase that a “further increase in interest rates cannot be ruled out”, Michele Bullock may use her press conference to explicitly discuss the risk of rate hikes given slow progress in taming inflation.

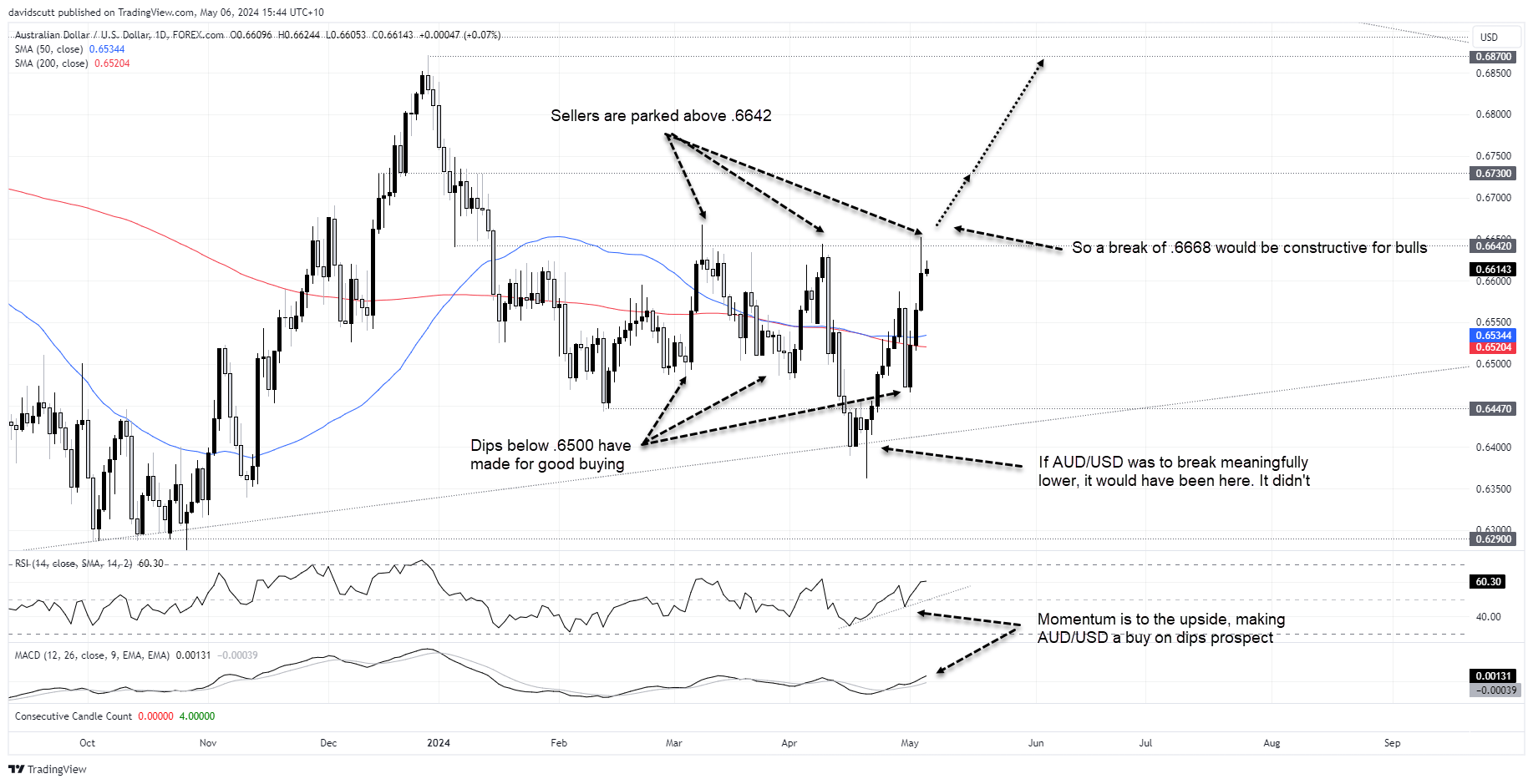

Looking to buy AUD/USD on dips

AUD/USD remains rangebound ahead of the RBA decision with momentum skewing higher.

Resistance starting from .6642 has capped advances on multiple occasions dating back to March, making this an important level to overcome for traders eying off a return to levels seen late last year. A break and close above the March 8 high of .6668 would be constructive, creating a potential run towards minor resistance at .6730 and December 2023 peak of .6870.

On the downside, dips below .6500 have been bought recently, the only exception being the middle of April when heightened geopolitical tensions in the Middle East and hawkish Fed rate pricing combined to push AUD/USD briefly below .6400. A repeat of those conditions appears highly unlikely near-term.

With price momentum skewing higher and US economic exceptionalism starting to be questioned, we prefer to buy dips rather than sell rallies right now.

-- Written by David Scutt

Follow David on Twitter @scutty

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 09:07 AM

Today 03:03 AM

Yesterday 11:02 PM

Yesterday 08:20 PM

Latest AUD articles

April 30, 2024 02:37 AM

April 24, 2024 06:51 AM

April 24, 2024 02:03 AM

April 22, 2024 10:40 PM