Q2 Forex Outlook: Dollar could weaken further

Our forex outlook for the rest of Q2 remains bearish on the US dollar against currencies where the central bank remains more hawkish than the Fed. We think that the ECB has more policy tightening work left, which should keep the US dollar undermined and the euro underpinned.

Calm returned to markets in the latter parts of March after SVB’s spectacular collapse and Credit Suisse’s takeover by UBS had led to a sudden jump in financial stability risks. The recovery continued through most of April, which meant Europe’s leading stock averages were either near or above levels from earlier this year. This helped to keep the dollar under pressure against the likes of the euro, while the safe-haven yen quickly lost its appeal as bond yields started to climb again as investors priced out expectations of interest rate cuts that had been priced in for as early as the start of Q4.

Forex outlook: ECB could hike rates 2 more times

As we move to the middle parts of Q2, one of the most aggressive central bank tightening cycles ever is reaching its final stages. We think that currencies where the central bank is relatively more hawkish should perform better than those where rate hiking is already paused or where the central banks is turning dovish.

Given that the ECB is likely to hike at least two more times this year, we think that the EUR/USD could climb towards the mid-1.10s. So our overall forex outlooks is that the Dollar Index will most likely remain in a downward trend.

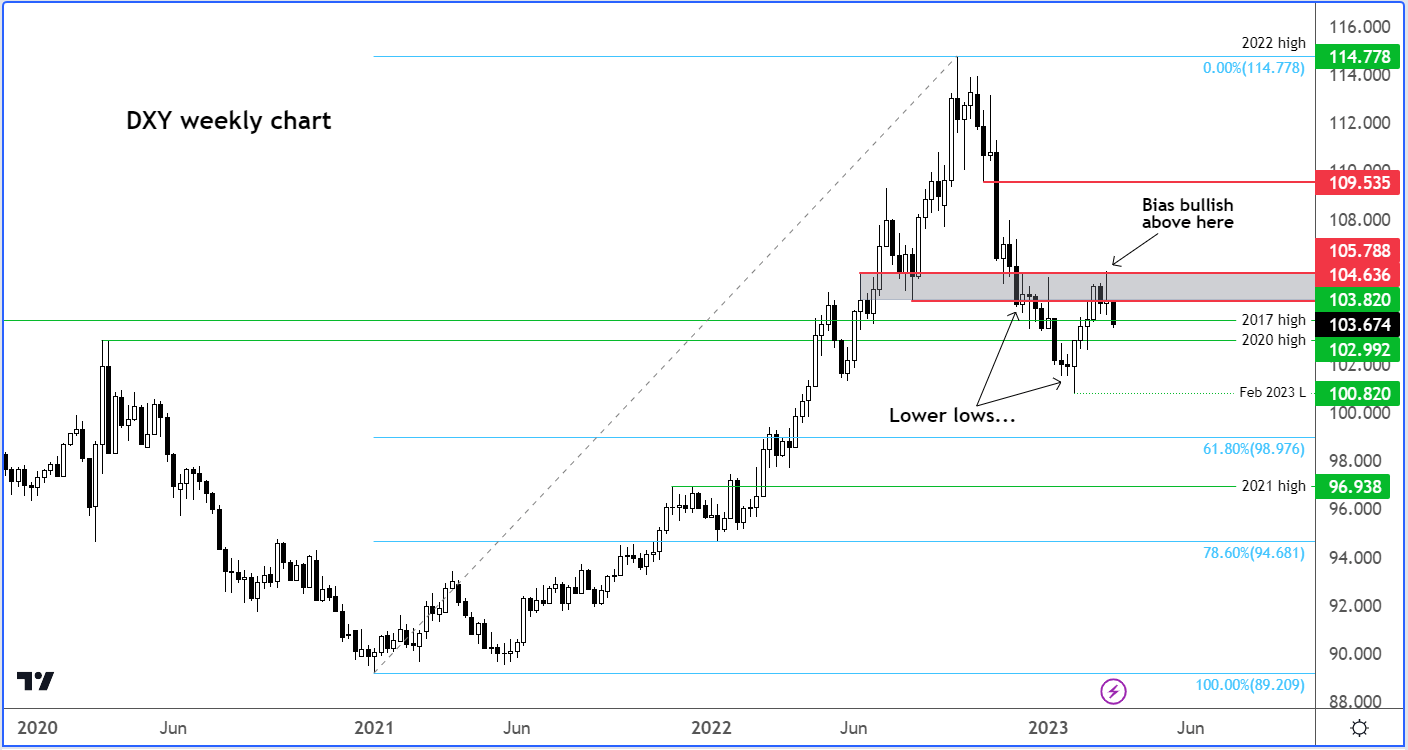

Tactically, we will maintain an overall bearish view on the dollar until something fundamentally changes to trigger a breakout above the trend resistance of the falling wedge pattern around 103.00 area. Even then, a higher above key resistance between in the 104.63 to 105.80 range would still be required to confirm a bullish reversal on the Dollar Index:

Forex outlook: Policy tightening impact to be felt on economy

For the dollar to regain renewed buying strength against its rivals in the coming quarter, we may need to see another acceleration in the rate of inflation. But headline CPI has been falling for 10 consecutive months, most recently dropping to a 5.0% annual pace in March.

The positive influences of a contractionary Fed policy have been mostly priced in. The negatives haven’t. High rates will be here for a while. They could hurt housing market activity as disposable incomes are squeezed even more. We could see more tech sector job cuts, leading to a rise in the unemployment rate… and eventually a sharper-than-expected slowdown in economic activity, and thus sooner-than-expected rate cuts – possibly as early as the end of this year.

Another negative influence for the dollar is the debt ceiling debacle. Funding has been secured until the end of Q2. Thereafter, it is possible the US government might default on its obligations. The ceiling is likely to be eventually raised again like every year, but that’s not to say it won’t impact investor sentiment towards US assets while the Democrats and Republicans try to call each other’s bluffs.

Forex outlook: Where are EUR/USD, GBP/USD and EUR/JPY headed?

For the reasons mentioned, it is difficult to be too positive on the dollar. We therefore expect currencies of countries where inflation is relatively high, economic activity mostly positive, and the financial stability risks low, to outperform. The likes of the eurozone and UK come to mind.

Consequently, we envisage a sustained breakout above 1.1000 on EUR/USD and think the GBP/USD will move north of 1.2500. The USD/JPY’s downside risks could be limited as the Bank of Japan is likely to maintain its previous policy settings under its new governor. We think the EUR/JPY could climb to 150.00, and thus reach its best levels since 2014.

Forex outlook: What is the key risk to our bearish dollar call?

One of the key risks to our bearish dollar call is if we see a sustained period of risk-off environment across the financial markets. The USD could benefit on haven flows in that case.

Written by Fawad Razaqzada, Market Analyst