The gold price is looking a little prematurely to the peak of the interest rate cycle. Seasonal December strength is historic, but do the fundamentals back it up this year? Technical considerations remain mixed but are supportive on balance. Gold and silver prices have been up 2.7% and 6.6%, respectively, since the start of last week – both are overbought in the short term.

Gold’s move above $2,000 late last week attracted attention because of the psychological significance of the prominent figure. Can it be sustained time? Several analysts point to the fact that gold typically enjoys price strength in December and suggest that this year will be the same. We agree but are slightly more cautious. Let’s consider the key factors.

|

|||||||||||||||||

| Source: StoneX. |

Conclusion

The bullish arguments outweigh the counterarguments, suggesting there is scope for further gains in December. But the market needs to slow or correct if this move is to prove sustainable and for the 2023 high ($2,063 intraday) to be removed.

Fundamentals

On a fundamental basis, there has been some sporadic price-related selling in southeast Asia, while India has gone quiet following the festival season. The latest trade figures from Hong Kong suggest reduced net exports into China in October, but this does not necessarily mean the Chinese market has contracted. Not all import quotas have been released, but by the same token, the domestic premium over the international market has recently come down from $40 to trade currently at $32, or just 1.6% of the spot price.

Gold: monthly moves over the past seven years; does this bode well for December and January?

Source: Bloomberg

Gold’s gain so far in November is just 1.4%, although this comes on top of a 7.3% October rise; on an intraday basis the rise for this quarter has been 8.9% (gold’s period of weakness came to an end in the first week of October at $1,180 sop the increase since then has been over $200 or 12%

Meanwhile it will be interesting to keep an eye on the Chinese ETPs. The increase in holdings so far this year have only been 7.4 tonnes but this is a 14% increase and potentially lays the foundation for expanding activity in the future.

Gold: scope for more upside, but a correction would add stability

Source: Bloomberg, StoneX

The fact that silver has moved by the times as much as gold in the past week gives further credibility to the move but here, too, the market is overbought and needs to correct. The physical market has also slowed, with premia coming right down in India, and continued regular supply from the base metal producers around the world, notably China and with BHP closing a deal with the miners’ union at its massive Escondida mine in Chile it looks as if output disruption in that country may now be on the retreat, but there is still strike action in Peru, at Southern Copper.

Gold, silver, the correlation, and the ratio: year-to-date

Source: Bloomberg, StoneX

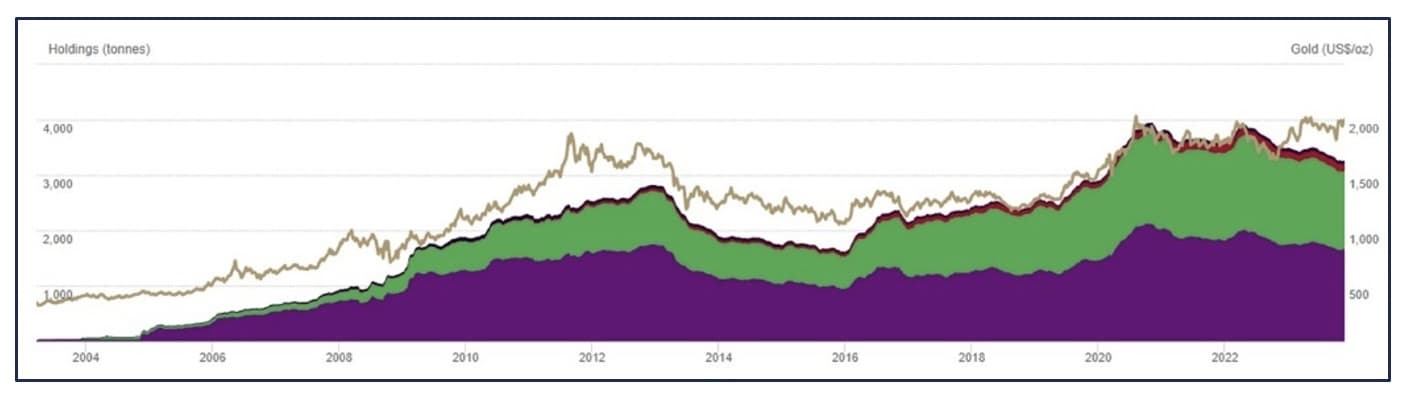

Exchange Traded Products

In the ETP sector, last week saw regional increases in holdings everywhere except North America, Germany and Switzerland, reflecting a growing, if very tentative, increase in investor interest notably in the UK and, interestingly, in China even though the latter was 58.8 tonnes, or 1.4%. The World Gold Council tracks over 100 such funds and pegs current holdings at 3,242.5 tonnes as of 24th November, meaning a year-to-date drop of 230.0 tonnes, or 6.6%.

ETF gold holdings by region

Source: World Gold Council

Silver has remained patchy, with eight days of net creations from a total of 18 trading days in November, although two of those were last week. The net change in November is a loss of 88 tonnes, and 1,249 tonnes tonnes year-to-date, or 5%, to stand at 22,047 tonnes; this compares with annual global mine production of approximately 26,000 tonnes.

Futures positioning

The numbers for the week to 21st November are not yet published due to the Thanksgiving Holiday in the US last Thursday, but or completeness we have kept the numbers from the previous week.

Gold price: dropped from $2,007 on 30th Oct to a low of $1,932 on the 13th the latest rally started on 13th and spot closed at $1,964.

Negative sentiment returning for the most part with longs down by 24 tonnes, or 5.5%, and shorts up 19.4 tonnes, or 10%. Net long down 18% to 200 tonnes from 243 tonnes and vs a 12-month average of 194 tonnes.

Gold COMEX positioning, Money Managers (tonnes)

Source: CFTC, StoneX

Silver price: dropped from $23.30 on 3rd November, bottomed at $21.88 on the 13th , and closed at $23.07 on the 14th.

Futures positioning in silver wasthe reverse of gold with a 20% (819 tonnes) increase in longs and a 5.1% (207 tonnes) contraction in shorts. Net long positions increased from 56 tonnes to 1,078 tonnes against a 12-month average of 1,761 tonnes.

Silver COMEX positioning, Money Managers (tonnes)

Source: CFTC, StoneX

Taken from analysis by Rhona O’Connell, Head of Commodity Market Analysis for EMEA & Asia, StoneX Financial Ltd.

Contact: Rhona.Oconnell@stonex.com.

Latest market news

Today 04:00 PM

Yesterday 08:00 PM

Yesterday 02:00 PM

Yesterday 07:00 AM

Yesterday 02:00 AM

December 24, 2024 08:00 PM

Latest US articles

October 3, 2024 04:38 PM

October 2, 2024 04:15 PM

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM